Inflation Watch - April 2022

This will be a thorough review of the inflation situation in the United States. The number one issue at the moment, economic or otherwise.

Oil

Before we slice into the meat of the inflation issue, let’s begin with a digression on oil prices. In my last post: Oil Prices and the War, I claimed that so long as the world’s oil production held up near 2019/2021 levels, oil prices couldn’t stay punishingly high.

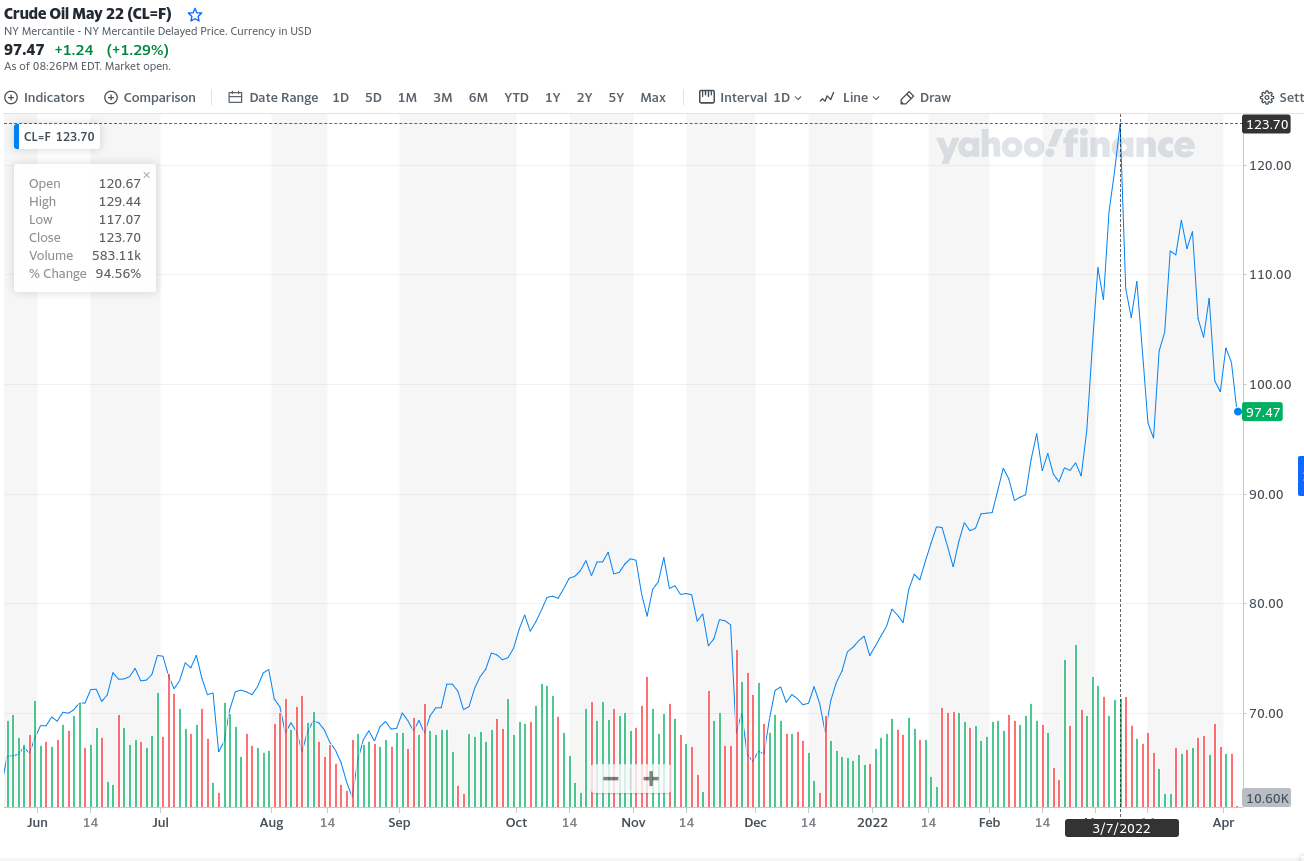

The chart below shows WTI futures prices for May ‘22 delivery. Before the SMO in the Ukraine, oil prices were “high”, at least relative to recent years, but not gruelingly so. Price rises before Feb ‘22, were driven by supply/demand dynamics, and anticipated dynamics. At the end of February the market priced in a sizable risk premium on oil deliveries, as the military operation, and resulting Sanctions Jihad by the USA and its satellites abruptly increased the odds of a disastrous war or retaliatory oil production embargo by Russia.

The WTI price peaked on March 7th at $123 per barrel, then rapidly dove down to $95 by March 15th. The price has since jarringly oscillated as the market worked to digest rapidly changing risks of a major supply disruption. This risk premium moves the price above the natural supply/demand equilibrium clearing price, causing inventories to build at a pace proportional to the risk premium.

Yesterday, the Energy Information Administration released their weekly petroleum report. The gist is that oil stockpiles increased more than expected, which sent the oil price from about $103 to about $97. You see while it is generally a good thing the private sector automatically hoards oil when there’s a risk of a disastrous supply disruption, there are hard limits on oil and oil product storage capacity. Once we hit those limits, supply will have to be sold at a steep discount. The market thus shaves down the risk premium as we approach storage limits.

Expect this pattern of intermittent price spikes, followed by abrupt returns toward a more normal price to continue through the summer. Traders are over the initial shock of the SMO, they understand its parameters, and that the Pentagon is not interested in fighting the Russians directly, so the risk premium is fairly modest now. Still, oil is priced above clearing, expect inventories to rise and slowly squeeze the premium out of the oil price.

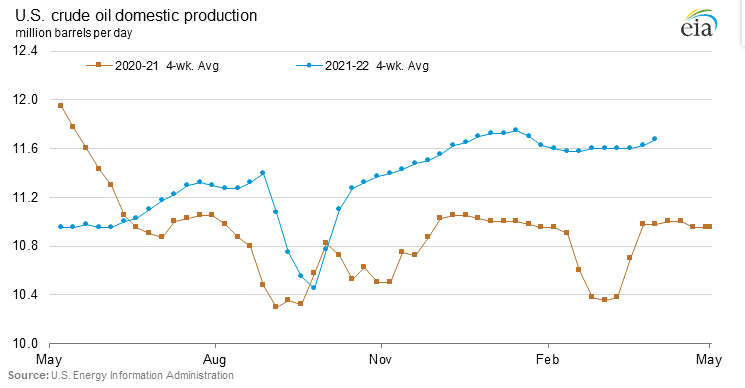

The last bit of news on oil is from the production side. US drillers cranked out a surprisingly large weekly increase in oil production. Just one data point but this is another reason a high risk premium is unsustainable: there’s simply too much scope currently for relatively low effort production increases in non-OPEC+ countries.

Demand-side Inflation

Let’s now get at the core of the inflation issue. Yes, the Russians are sanctioned, yes the economic war could get worse, but the inflation issue predates the Ukraine situation by at least a year. The inflation we’ve seen the past 18 months was not principally driven by market anxiety surrounding petroleum products. Instead, inflation is readily explained by a conventional demand-side story: too much money is being spent, retailers are overloaded with sales, so they raise prices.

Let’s have a look at our old friend, the retail trade chart for the USA

The chart shows us monthly retail sales in millions of USD (no inflation adjustment). The series moves around a little month to month, but in general retail sales in the USA hold on surprisingly steady trendlines between recessions. The first trend line in the chart is about 5% growth per year, from 1992 to the end of 2007. Then we have the great recession, and the establishment of a new trend line, holding at about 4% per year, from Jan-2010 through Feb-2020. Those of you who are in the NGDP watching game will note retail sales basically match the trend lines for NGDP as well.

The US Federal Reserve (Fed) is ultimately responsible for managing the flow of spending through the US economy. Yes, the private sector and the government can influence the flow of spending. But they influence it in the same way a moderately sized dog influences his path on a walk with his owner. The dog can stray away from his owner, if his owner is a total wimp the dog can dominate, but if the owner has even a little will and strength, the owner (the Fed) will ultimately decide the pace and path of the walk.

The Fed doesn’t directly target retail sales, but they certainly do more or less target inflation, and the way to stabilize inflation is to stabilize nominal spending aggregates, like domestic demand, like nominal GDP, like retail sales. That’s why the line is so predictable, holds to trend lines for so long.

If the Fed had been content to see us back on the boring, safe, 4% trend line following the corona hysteria that began in March 2020, we’d currently have about $497 billion in monthly retail sales. Instead, we have $584 billion. This means we are ***17%*** above where a reasonable forecaster would have put us, prior to the Corona virus travesty.

The chart below shows what I’m talking about. The solid black line is measured retail sales, the dashed line at the end shows the reasonable forecast of what we “should have” seen, starting in March 2020.

The Inflation Outlook

On the even of the Corona hysteria, 5-year inflation breakevens were about 1.7%. That’s a market forecast for about 1.7% inflation per year, for five years. Such an inflation outlook was characteristic of the period between The Great Recession and Corona; 0.2-0.6 percentage points below the Fed’s 2.0% target. On the eve of the Russian campaign, before any risk premium was priced into TIPS, 5-year breakevens had shot up to 2.8%. They’ve shot up more since, basically for the same reason oil prices have. This pre-Ukraine inflation outlook surge was almost entirely due to huge increase in household spending, brought on by excessively stimulative fiscal and monetary measures introduced in the name of fighting the virus.

How did we get here?

Ultimately only a few powerful insiders really know why the Fed allowed the economy to get so hot, why they let 5-year inflation expectations soar up to 2.8%, a full 40% above the Fed’s own target, and after the Fed has already made up for the systematic inflation shortfalls accrued during the Bernanke and Yellen years by running the economy red-hot through 2021. I consider two scenarios most likely:

A deal was made to run the US economy hot for a few years. The incompetent and unpopular “Biden” administration and corona fallout could be blamed. The benefits would be to inflate away some of the US debt before the Chinese fully divest, and to boost tax revenues through higher NGDP growth and associated, partly inflation-driven capital gains tax bonanza. Powerful interests who might be harmed by unexpected inflation would be tipped off ahead of time and able to gain from insider trading.

The Fed over-did it. The Fed truly wanted to correct its excessively low-inflation policy of the Bernanke and Yellen years, and bring about a period of above-2% inflation, as compensation for years of sub 2% inflation. However, while things worked great through mid 2021, the Fed’s internal models didn’t account for retail-stimulating nature of fiscal policies like early child tax credit disbursements and suspended student loan payments. The administration surprisingly extended the student loan payment jubilee, breaking informal agreements with the FOMC, and households misunderstood the nature of the early child tax credit disbursements, anticipating another disbursement after sending in their 2021 taxes.

These and other factors combined to extend the consumer spending binge into latter 2021 and into 2022, to an extent the Fed never intended.

As you can see, I’m torn between cynicism and a mundane bureaucratic story. I put a 30% weighting on story 1, and a 70% weighting on story 2. Especially after yesterday’s (6-April-2022) bearish FOMC statement sent stocks, oil and crypto lower, I think we can be more confident the Fed will finally throw cold water on the economy. One wonders if today’s policy tightening statement (market expectations are de facto policy) isn’t payback for the Biden regime’s announcement that student loan payment holiday would be extended through August 2022.

I will not be selling any assets, but I will start holding surplus income as cash, betting that the Fed will seek to shave 0.3 to 0.5 percentage points off the 5-year breakeven this year. This would be done by implicitly lowering the expected path of NGDP from maybe 5.5% per year to 5.0-4.5% per year. Such a path change means $200-odd billion less NGDP per year, which is bound to weigh on stocks. I could be wrong, I was wrong last year thinking the Fed would tightening in the Fall. Still, it’s more likely than not the FOMC come to their senses and back off from their current reckless expansionary policy.